El Paso Native American Mortgage Lender

Native American Home Loans In El Paso

The Section 184 Indian Home Loan Guarantee Program is a mortgage loan program developed exclusively for American Indian and Alaska Native households, Alaska villages, tribes, and tribally designated housing institutions. Congress launched this program in 1992 to increase access to capital and facilitate homeownership in Native American communities.

The Housing and Community Development Act of 1992 created the Section 184 Loan Guarantee Program to make it easier for Native Americans who live on reservations to obtain a mortgage. Section 184 financing enables borrowers to purchase a property with a small down payment and flexible underwriting. Section 184 loans may be utilized for new construction, rehabilitation, purchasing an existing home, or refinancing on and off native grounds.

What is HUD Section 184?

Section 184 was enacted to provide private lenders with the necessary insurance to offer mortgage loans on reservations. Section 184 loans are developed exclusively for American Indian and Alaska Native families, Alaska Villages, Tribes, and tribally designated housing entities.

The Office of Native American Programs administers them within the US Department of Housing and Urban Development. These loans may be utilized for new construction, rehabilitation, acquiring an existing home, or refinancing on or off tribe territory. Due to the special status of Indian lands, Section 184 is a program tailored specifically to tribal communities.

How does HUD Section 184 work?

Section 184 home mortgage loans issued to Native borrowers are backed by the Office of Loan Guarantee inside HUD’s Office of Native American Programs. The loan guarantee guarantees the full repayment of the lender’s investment in the event of foreclosure.

If the property is on tribal trust land, the qualified buyer collaborates with HUD and the Bureau of Indian Affairs to set up the house as a leasehold estate, making it a leased entity for the life of the mortgage plus an additional ten years. The mortgage requires approval from both departments, and in the event of a default, the lender will take possession of the lease rather than the actual property. The lender is not permitted to sell the property to anybody other than an eligible tribe member, the Tribe, or the Indian Housing Authority because it still belongs to the Tribe and is a part of the Trust.

The loan is restricted to single-family homes and loans with fixed rates of 30 years or less. The HUD Section 184 Indian Home Loan Guarantee program is for primary residence only. Commercial properties and adjustable-rate mortgages (ARMs) are ineligible for Section 184 financing. The maximum loan amount varies per county.

Who is Eligible for HUD Section 184 Home Loans?

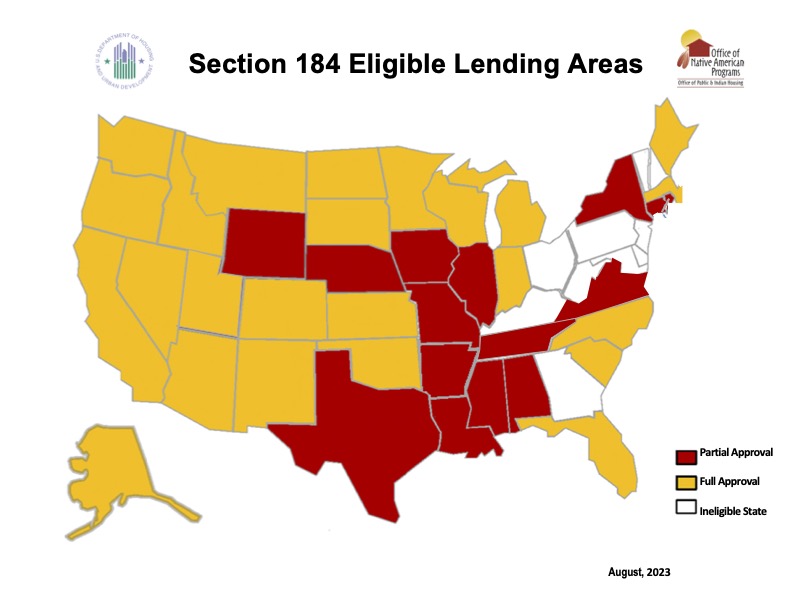

To qualify for a Section 184 loan, you must be a member of a federally recognized Native American or Alaskan tribe. Enrollment into a tribe is determined entirely by the tribal authority, which will often produce a card or letter verifying enrollment. When applying for a Section 184 loan, proof of tribal membership will be required. The participating Tribes are permitted to select whether Section 184 eligibility is confined to specific counties or encompasses the entire state.

Apply for Section 184 Loan with Capital Home Mortgage

Capital Home Mortgage is a direct lender and servicer in Texas. Call us at (915) 283- 3949 to speak with our Home Loan Specialists about Native American Home Loans in El Paso.

Why El Paso HomeBuyers are Choosing Capital Home Mortgage

Close On Time

Complete Control from Application to Funding

Low Rates & Low Fees

Direct Lender with Competitive Rates & Low Fees

Exceptional Service

7 Day a Week Support Application to Final Mortgage Payment

El Paso Mortgage Rates

Have you ever wondered why interests rates are what they are and what determines the final rate? Why borrowers receive different interest rates? Or why rates go up and down? Interest Rates are calculated using several factors.

- Demand for mortgage Securities

- Property securing the mortgage

- occupancy of the property

- Loan to value of the property

- Borrower’s credit worthiness

El Paso Native American Purchase Loans

- Primary Residences Only

- Manual Underwriting for All Loans

- No Credit Score Requirements

- Tribal Grants Allowed

- Purchase an Existing Home

- Construction of a New Home

- Rehab an Existing Home

- Purchase / Rehab Combo Loan

El Paso Native American REfinance Loans

CAsh-Out or Renovation

- Appraisal Required

- 97.75% Max LTV for Rehab

- 85% Max LTV for Cash-out

- County Loan Limits Apply

Streamline REfinance

- HUD 184 to HUD 184

- No Income Qualification

- No Appraisal Required

- No Mortgage Lates in Last Year

Texas Mortgage Programs

Texas Home Purchase

Thinking of Buying a Texas Home?

Looking to Purchase a Home? We have the loan program for you… Call today to speak with a loan officer to discuss your personal mortgage options.

- Primary, Secondary, Investment

- FHA, VA, USDA, Native American

- Conventional, Jumbo, Non QM

- Reverse, Renovation, Manufactured

Texas renovation home loans

Looking to Rehab a Texas Home?

Want the Charm of an Older Neighborhood? But want a new place or a fresh look? Why not look at a renovation loan? Purchase the Perfect Home and make it your own. Call today.

- Remodel, Renovate or Repairs

- FHA 203K Streamline or full

- fannie mae homestyle reno

- freddie mac home choice reno

Texas FHA Home Loans

Great for 1st Time Texas Homebuyers

FHA Home Loans are great for first time home buyers, buyers with less than perfect credit, or buyers needing less out of pocket. Call today to get started.

- Smaller Down Payment

- Flexible Underwriting

- Higher Debt to Income Ratios

- Lower Credit Scores OK

Texas VA Home Loans

100% Financing for Texas Veterans

Proudly Serving Active Duty servicemen and women, as well as, retired and disabled veterans. Call today to speak with a VA loan officer.

- Simply Qualifying for Veterans

- No Down Payments Requirements

- Lower Credit Scores Accepted

- Manual Underwriting Allowed

Texas Conventional Home Loans

Flexibility for Texas Homebuyers

Conventional Home Loans are the best option for flexibility of property types and for mortgage loan terms. Call today to get speak to a Loan Officer.

- Primary, 2nd Home, Investment

- Great Rates & Low Fees

- Single Family and Multi-Family

- Renovation Loan Programs

Texas Jumbo Home Loans

Texas Non Conforming Loans

Jumbo Home Loans also called Non Conforming Home Loans are great options for buyers needing financing outside of agency limits. Call today to speak to a loan officer.

- Primary Residence and 2nd Homes

- Higher Loan Amounts – 3 Million

- Great Interest Rates

- Investor Specific Guidelines

Texas USDA Home Loans

100% Rural Texas Home Loans

USDA Loans are a great option for families wanting to live outside of the city. Call today to speak with a loan officer to discuss your personal loan options.

- Rural Properties Only

- Primary Residence Only

- Geographic Restrictions

- Income REstrictions

Texas Native American Home Loans

Texas HUD 184 Home Loans

HUD 184 Home Loans are solely for Native American and offer a variety of benefits. Call today to speak with a loan officer to find out more.

- Primary Residence Only

- Manual Underwriting for All Loans

- No Credit Score Requirements

- Tribal Grants Allowed

Texas reverse mortgages

Your Texas Home at Work

Reverse Mortgage Loans offer seniors options to use their home’s equity for cash or to eliminate payments. Call today to get speak to a Reverse Loan Officer.

- primary residence only

- simple qualifying – equity based

- credit scores not applicable

- Minimum age 62

Texas Non QM Home Loans

Making Texas Mortgages Possible

Looking for Non Traditional Home Mortgage Loan? Contact a Loan Officer Today to discuss the alternative mortgage options currently available.

- Purchase, Rate and Term & Cash-out

- Primary, Secondary and Investment

- Full Doc & Bank Statements Programs

- Corporations OK

Texas One Time Close mortgages

Build Your Texas Dream Home

Want to Build? But unsure of what the future looks like? Remove the risk with a One Time Close Construction Loan. Call today to see how a OTC loan works.

- Primary Residence Only

- Close Once

- Lock Rate at Contract

- Traditional Final Mortgage

Texas Refinance Mortgage Loans

Texas Rate & Term Refinance

Refinancing can be a hard decision and the payback can sometimes be confusing. Call today and let our Loan Officers walk you through the process.

- Reduce Mortgage Term

- Lower Monthly Payments

- Appraisal Waivers

- Streamline Options Available

Texas Cash-out Home mortgages

Texas Equity Mortgage Loans

Cash-Out Mortgage Loans make use of the equity in your home by allowing you to refinance the current mortgage and access this equity to use as you see fit.

- Debt Consolidation

- Investment Opportunities

- Home Improvement

- Vacation or Education