Midland Native American Mortgage Lender

Midland Native American Loans

Homeownership is a cornerstone of the American dream and is widely seen as a sound financial investment. However, Native Americans have not always had access to this opportunity, as mortgage lenders seldom provide loans to people living on reservations or federal trust lands.

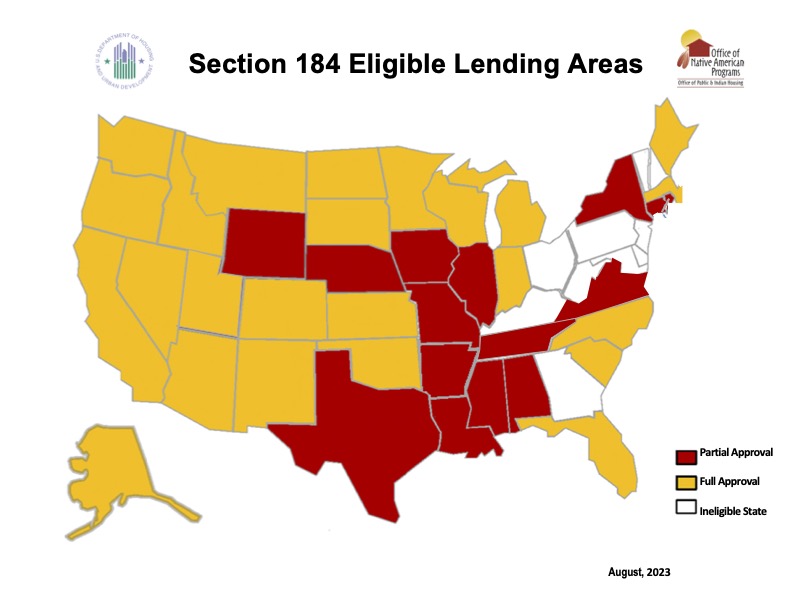

But thanks to the Section 184 Indian Home Loan Guarantee Program, American Indians and Alaska Natives can now obtain mortgage loans for homes on or off Native lands.

What is the HUD Section 184 Loan?

The Section 184 Native American Home Loan Guarantee Program was established in 1992. The program aims to make homeownership more accessible to Native Americans by offering loan guarantees to lenders looking to provide home loans to Native Americans. The guarantee protects the interests of lenders in case of foreclosure, reducing their risk.

Who is Eligible For Native American Home Loan?

Eligibility for the Section 184 Loan Program is contingent upon possessing a valid tribal membership or citizenship card issued by a federally recognized tribe. This loan option is NOT reserved for first-time buyers, so all Native American members of a federally recognized tribe are eligible.

Why Choose HUD Section 184 Loan?

The Section 184 Loan Program is the best option for American Indians and Alaska Natives seeking to buy a home in Midland, Texas, or anywhere else in the state. Here are several compelling reasons why:

1. Specifically created for Native Americans

HUD-184 was explicitly established to offer home and housing renovation loans to Native Americans and Alaskan Native individuals and families.

Although the program has a few basic requirements that applicants must meet to qualify for a loan, it offers generous allowances and is easier to obtain than a conventional loan.

2. Easier qualification process

One thing that makes HUD-184 loans unique is that each application is reviewed and manually underwritten by a home loan specialist. The program also makes exceptions for borrowers who do not meet the standard requirements set forth by banks and mortgage lenders due to a lack of credit or a history of credit problems.

3. Lower down payment

A down payment of between 5% and 20% is typically required for a conventional mortgage, while the down payment requirement for an FHA loan is 3.5%. The HUD-184 requires an even smaller down payment than the previous two. The minimum down payment for Section 184 loans over $50,000 is 2.25%, while loans under $50,000 require only 1.25%.

4. No income limits or credit score requirements

There are no credit requirements for a Section 184 loan, which is a huge plus. You can still qualify for this loan even if you have a low or nonexistent credit history because each application is evaluated on its merits. Moreover, there is no need to worry about a minimum or maximum income requirement.

5. Great mortgage rates

Market rates, not an applicant’s credit score, determine the interest rate for HUD-184 loans, so borrowers can rest assured that they will always receive a competitive rate. This program’s funding fees and mortgage insurance premiums are significantly lower than those of FHA-backed loans.

6. Flexible down payment and versatile financing options

The down payment for a Section 184 loan can come from various sources. You can utilize personal savings, gifts from relatives or friends, or tribal grants or aid. Furthermore, the Section 184 Native American Home Loan Program can finance home purchases, new construction, renovations or rehabilitations, or refinancing existing mortgages.

Start Your Homeownership Journey With Capital Home Mortgage

The HUD Section 184 program has many great features that set it apart from other loan programs. If you qualify for a Section 184 loan, there’s no reason not to take advantage of it. For HUD-184-eligible Midland homebuyers, the process starts by speaking with one of our home loan officers at Capital Home Mortgage.

We are a direct mortgage lender, experienced in handling HUD-184 loans and other conventional and government-guaranteed mortgages. With us, you can rest assured that you’ll receive the information and guidance to navigate the mortgage process successfully.

Need more information about the HUD Section 184 Native American Home Loan? Contact us at (432) 218-4828 now!

Why Midland HomeBuyers are Choosing Capital Home Mortgage

Close On Time

Complete Control from Application to Funding

Low Rates & Low Fees

Direct Lender with Competitive Rates & Low Fees

Exceptional Service

7 Day a Week Support Application to Final Mortgage Payment

Midland Mortgage Rates

Have you ever wondered why interests rates are what they are and what determines the final rate? Why borrowers receive different interest rates? Or why rates go up and down? Interest Rates are calculated using several factors.

- Demand for mortgage Securities

- Property securing the mortgage

- occupancy of the property

- Loan to value of the property

- Borrower’s credit worthiness

Midland Native American Purchase Loans

- Primary Residences Only

- Manual Underwriting for All Loans

- No Credit Score Requirements

- Tribal Grants Allowed

- Purchase an Existing Home

- Construction of a New Home

- Rehab an Existing Home

- Purchase / Rehab Combo Loan

Midland Native American REfinance Loans

CAsh-Out or Renovation

- Appraisal Required

- 97.75% Max LTV for Rehab

- 85% Max LTV for Cash-out

- County Loan Limits Apply

Streamline REfinance

- HUD 184 to HUD 184

- No Income Qualification

- No Appraisal Required

- No Mortgage Lates in Last Year

Texas Mortgage Programs

Texas Home Purchase

Thinking of Buying a Texas Home?

Looking to Purchase a Home? We have the loan program for you… Call today to speak with a loan officer to discuss your personal mortgage options.

- Primary, Secondary, Investment

- FHA, VA, USDA, Native American

- Conventional, Jumbo, Non QM

- Reverse, Renovation, Manufactured

Texas renovation home loans

Looking to Rehab a Texas Home?

Want the Charm of an Older Neighborhood? But want a new place or a fresh look? Why not look at a renovation loan? Purchase the Perfect Home and make it your own. Call today.

- Remodel, Renovate or Repairs

- FHA 203K Streamline or full

- fannie mae homestyle reno

- freddie mac home choice reno

Texas FHA Home Loans

Great for 1st Time Texas Homebuyers

FHA Home Loans are great for first time home buyers, buyers with less than perfect credit, or buyers needing less out of pocket. Call today to get started.

- Smaller Down Payment

- Flexible Underwriting

- Higher Debt to Income Ratios

- Lower Credit Scores OK

Texas VA Home Loans

100% Financing for Texas Veterans

Proudly Serving Active Duty servicemen and women, as well as, retired and disabled veterans. Call today to speak with a VA loan officer.

- Simply Qualifying for Veterans

- No Down Payments Requirements

- Lower Credit Scores Accepted

- Manual Underwriting Allowed

Texas Conventional Home Loans

Flexibility for Texas Homebuyers

Conventional Home Loans are the best option for flexibility of property types and for mortgage loan terms. Call today to get speak to a Loan Officer.

- Primary, 2nd Home, Investment

- Great Rates & Low Fees

- Single Family and Multi-Family

- Renovation Loan Programs

Texas Jumbo Home Loans

Texas Non Conforming Loans

Jumbo Home Loans also called Non Conforming Home Loans are great options for buyers needing financing outside of agency limits. Call today to speak to a loan officer.

- Primary Residence and 2nd Homes

- Higher Loan Amounts – 3 Million

- Great Interest Rates

- Investor Specific Guidelines

Texas USDA Home Loans

100% Rural Texas Home Loans

USDA Loans are a great option for families wanting to live outside of the city. Call today to speak with a loan officer to discuss your personal loan options.

- Rural Properties Only

- Primary Residence Only

- Geographic Restrictions

- Income REstrictions

Texas Native American Home Loans

Texas HUD 184 Home Loans

HUD 184 Home Loans are solely for Native American and offer a variety of benefits. Call today to speak with a loan officer to find out more.

- Primary Residence Only

- Manual Underwriting for All Loans

- No Credit Score Requirements

- Tribal Grants Allowed

Texas reverse mortgages

Your Texas Home at Work

Reverse Mortgage Loans offer seniors options to use their home’s equity for cash or to eliminate payments. Call today to get speak to a Reverse Loan Officer.

- primary residence only

- simple qualifying – equity based

- credit scores not applicable

- Minimum age 62

Texas Non QM Home Loans

Making Texas Mortgages Possible

Looking for Non Traditional Home Mortgage Loan? Contact a Loan Officer Today to discuss the alternative mortgage options currently available.

- Purchase, Rate and Term & Cash-out

- Primary, Secondary and Investment

- Full Doc & Bank Statements Programs

- Corporations OK

Texas One Time Close mortgages

Build Your Texas Dream Home

Want to Build? But unsure of what the future looks like? Remove the risk with a One Time Close Construction Loan. Call today to see how a OTC loan works.

- Primary Residence Only

- Close Once

- Lock Rate at Contract

- Traditional Final Mortgage

Texas Refinance Mortgage Loans

Texas Rate & Term Refinance

Refinancing can be a hard decision and the payback can sometimes be confusing. Call today and let our Loan Officers walk you through the process.

- Reduce Mortgage Term

- Lower Monthly Payments

- Appraisal Waivers

- Streamline Options Available

Texas Cash-out Home mortgages

Texas Equity Mortgage Loans

Cash-Out Mortgage Loans make use of the equity in your home by allowing you to refinance the current mortgage and access this equity to use as you see fit.

- Debt Consolidation

- Investment Opportunities

- Home Improvement

- Vacation or Education