Capital Home Mortgage Alabama

Alabama Home Loans

Alabama Mortgage Lender

Home Loans in Alabama

Welcome to Capital Home Mortgage Alabama, where our goal is to provide Alabama Home Loans to Alabama homebuyers and homeowners with low rates and fees while providing exceptional service.

First, we want to thank you for the opportunity to earn your business. We understand that purchasing a home is the biggest decision of the most people lives and that is why Capital Home Mortgage Alabama provides dedicated points of contact throughout the entire mortgage process. This ensures a stress-free smooth experience finishing with an on time closing. After all buying a home should be exciting, not stressful.

As a direct Alabama Mortgage Lender, Capital Home Mortgage Alabama controls the lending process from start to finish. Our in house processing and underwriting allows for quick make sense approvals and on time closings. This control means from application to funding we make every decision.

Capital Home Mortgage Alabama is a full service Alabama Mortgage Lender that offers a wide range of mortgage products as well as competitive Alabama Mortgage Rates. Whether you are a first-time purchaser seeking an Alabama FHA Home Loan, looking for a rural property and needing an Alabama USDA Home Loan, Native Alabamian wanting to use the HUD 184 Alabama Native American Home Loan, an active or retired veteran in need of an Alabama VA Home Loan, or a seasoned buyer in need of an Alabama Conventional Home Loan, we are here to assist.

Call today (205) 352-1030 to speak with our Alabama Loan Officers.

Alabama, is known for its rich history, Southern hospitality, diverse culture, and natural beauty. Montgomery is the capital city, while Birmingham is the largest city in the state. Alabama played a significant role in the civil rights movement and is home to various historical landmarks associated with that period. The state also boasts scenic landscapes, including the Gulf Coast beaches, the Appalachian Mountains in the northern part, and numerous rivers like the Tennessee River.

Alabama’s real estate market has shown steady growth in recent years. Cities like Birmingham, Huntsville, and Mobile have seen increased demand for residential properties. The state offers a diverse range of housing options, from urban apartments to suburban homes and rural properties. Factors such as job growth, a relatively low cost of living, and favorable weather contribute to its attractiveness for homebuyers and investors. Whether you’re looking for a starter home, investment property, or commercial real estate, Alabama provides various opportunities across its regions.

Alabama is located in the Southeastern region of the United States, with Tennessee and Georgia to the north, Florida and the Gulf of Mexico to the south, and Mississippi to the west. Alabama is the 30th largest state by land area and the 24th most populous state in the United States.

Thank you again for allowing us to help you with your Alabama Home Loan

Alabama Home Loans

Alabama Conventional Home Loans

Alabama FHA Home Loans

An Alabama FHA Home Mortgage is a mortgage insured by the Federal Housing Administration or “FHA” and issued by an FHA-approved lender. FHA loans are designed for low-to-moderate-income applicants and first time homebuyers who need a smaller down payment. However, FHA home loans can be used by anyone.

FHA home loans feature a low down payment, flexible credit score requirements and the ability to use gift funds for the down payment. Other eligibility requirements for an Alabama FHA home loan is consistent employment history and documented income.

Alabama VA Home Loans

Alabama USDA Home Loans

Alabama Jumbo Home Loans

Alabama Non QM Home Loans

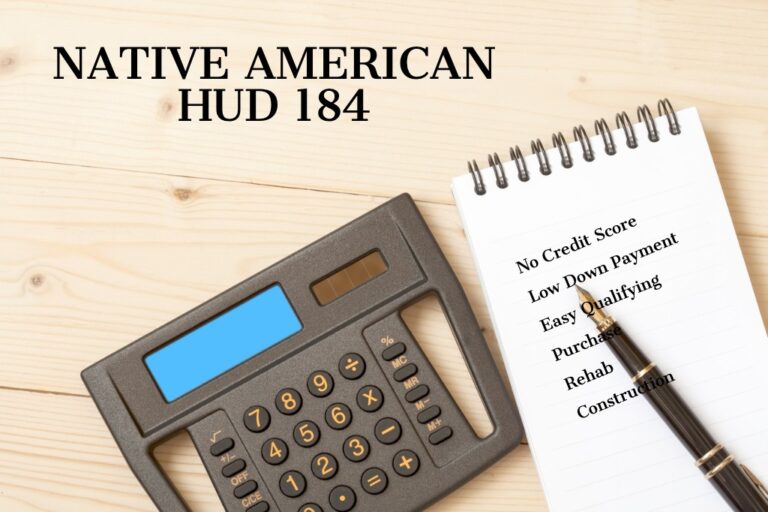

Alabama Native american Home Loans

An Alabama Native American Mortgage, also known as a HUD 184 Home Loan, is a government mortgage loan specifically for registered Alabama Native Americans. This loan offers easier credit qualifications, tribal grants and can be used to renovate the home along with the purchase.

Alabama One Time Close construction Home Loans

Why Alabama HomeBuyers are Choosing Capital Home Mortgage

Close On Time

Complete Control from Application to Funding

Low Rates & Low Fees

Direct Lender with Competitive Rates & Low Fees

Exceptional Service

7 Day a Week Support Application to Final Mortgage Payment

Alabama Mortgage Rates

Have you ever wondered why interests rates are what they are and what determines the final rate? Why borrowers receive different interest rates? Or why rates go up and down? Interest Rates are calculated using several factors.

- Demand for mortgage Securities

- Property securing the mortgage

- occupancy of the property

- Loan to value of the property

- Borrower’s credit worthiness

Alabama Mortgage Programs

Alabama Home Purchase loans

Looking to Purchase an Alabama Home?

- Primary, 2nd Home, Investment

- Low Rates & Fees, No fee Options

- FHA, VA, USDA, Native American

- Conventional, Jumbo & Renovation

- Manufactured, Construction, Reverse

Alabama Renovation Home Loans

Looking to Rehab an Alabama Home?

- Remodel, Renovate or Repairs

- FHA 203K Streamline

- FHA Full Documentation Rehab

- Fannie Mae Homestyle Reno

- Freddie Mac Home Choice Reno

Alabama FHA Home loans

Great 1st Time Alabama Homebuyers

- Smaller Down Payments

- Flexible Underwriting Guidelines

- Higher Debt to Income Allowed

- Lower Credit Scores – Down to 500

- Down Payment Gifts Allowed

Alabama va Home Loans

100% Financing for Alabama Vets

- No Mortgage Loan Limits

- Simple Qualifying

- Higher Debt to Income Allowed

- Lower Credit Scores – Down to 500

- Manual Underwriting Allowed

Alabama Conventional Home loans

Flexibility for Alabama Homebuyers

- Primary, 2nd Home, Investment Properties

- Single and Multi-Family Properties

- Variable Mortgage Insurance Options

- Low Rates & a Variety of Mortgage Terms

- Renovation Programs Available

Alabama Jumbo Home Loans

Alabama Non-Confirming Home Loans

- Primary & 2nd Homes

- Variety of Mortgage Programs

- Simple Qualifying for Veterans

- Investor Specific Guidelines

- Credit Score Minimums

Alabama USDA Home loans

100% Rural Alabama Home Loans

- Primary Residences

- No Down Payment Required

- New Manufactured Homes Allowed

- Closing Costs / Repairs Rolled In

- Geographic and Income Limits Apply

Alabama Native american Home Loans

Alabama Hud 184 Home Loans

- Primary Residence Only

- Manual Underwriting for All Loans

- No Credit Score Requirements

- Tribal Grants Allowed

- Purchase, Refinance, and Renovation

Alabama Manufactured Home loans

Great Alternative Alabama Housing

- Existing Purchase or Refinance

- New Construction

- One Time Close Land/Home Combo

- Lock at Contract

- FHA, VA, USDA, Native American

Alabama Reverse Mortgage Loans

Your Alabama Home at Work

- Primary Residence Only

- Simple Qualifying – Equity Based

- No Credit Score Requirements

- Minimum Age 62

- Purchase, Refinance, and Cash-Out

Alabama Non QM Home loans

Making Alabama Mortgages Possible

- Purchase, Refinance & Cash-out

- Primary, Secondary, Investment Properties

- Full Doc Programs

- Alt Doc Programs

- Corporations OK

Alabama One Time Close Home Loans

Build Your Alabama Dream Home

- Primary Residences Only

- One Time Close

- Lock Rate at Closing

- Traditional Final Mortgages

- No Payments During Construction

Alabama Refinance Mortgage loans

Alabama Rate & Term Refinance

- Lower Monthly Payment

- Shorten Mortgage Term

- Streamline Options Available

- Appraisal Waivers Allowed

- VA IRRRL’s

Alabama Cashout Mortgage Loans

Alabama Equity Mortgage Loans

- Debt Consolidation

- Investment Opportunities

- Home Improvement

- Dream Vacation

- Higher Education